A Better Health Insurance Market For Oregon

Options for Oregon to Maintain Consumer Access to Affordable Health Insurance

New report from OSPIRG Foundation and Frontier Group details rising health care costs and federal disruptions to the individual insurance market; explores policy options to stabilize prices and expand consumer choice.

The rising cost of health care is driving up the cost of insurance for all consumers, especially for those who buy insurance through the individual market. The federal Affordable Care Act (ACA) included measures to create a stable insurance market where individual consumers could obtain affordable, comprehensive insurance. However, as the federal government has lessened its support of the health care law, the market for individual insurance has weakened, limiting consumers’ ability to obtain comprehensive insurance at a reasonable price.

Oregon can adopt a number of policies to help stabilize the individual insurance market, which is important for those who currently buy insurance there and those who might need to do so in the future. Oregon can stabilize the market by reducing uncertainty and risk for insurers and encouraging healthier consumers to continue to buy insurance coverage. To achieve long-term stability for all consumers, however, Oregon must also pursue options for reducing the high cost of health care.

Health care is expensive, with prices rising annually. This means that insurance is also growing more expensive.

In 2014, $31.9 billion was spent on health care in Oregon, an average of $8,000 per person.[i] Since then, national-level data show that expenditures increased by 5.9 and 4.3 percent in 2015 and 2016, respectively.[ii]

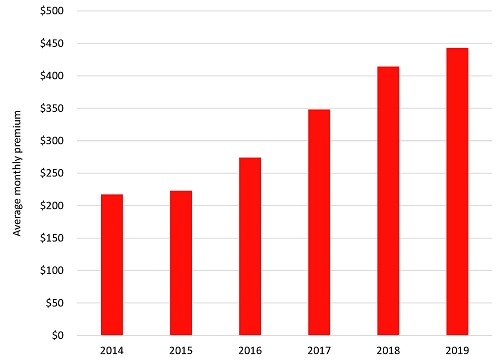

Oregonians who buy insurance for themselves and their families without the help of an employer or public program face high and rising costs. The average monthly premium for the second-cheapest “silver” level plan in Oregon’s individual marketplace is $443 in 2019, nearly double what it was in 2014 (see Figure ES-1).[iii]

After multiple unsuccessful attempts to repeal the ACA, Congress instead eliminated the penalty that enforced the individual mandate that individuals have health insurance.[ix] Multiple insurers in Oregon cited the loss of the individual mandate as a factor in why they proposed higher rates in 2019.[x]

Several federal risk-reduction programs that helped protect insurers from unexpectedly high costs have ended, potentially exposing insurers to greater expenses and greater uncertainty. Three insurers who had participated in Oregon’s individual insurance market in the first several years of the ACA ended or scaled back their offerings after the federal government withdrew promised financial support for insurers.[xi]

Insurers no longer receive a cost-sharing subsidy for providing plans to lower income customers, but still must sell those plans. Through an approach called “silver loading,” insurers have increased premiums on other customers to cover their costs, meaning that thousands of Oregon customers who do not qualify for tax credits to offset higher premiums are now paying more for insurance.[xii]

The federal government has eased rules on health plans that do not comply with ACA requirements. This allows insurers to sell plans with less comprehensive coverage.[xiii] Oregon has imposed significant restrictions on such plans that may curtail their impact in the state, though such plans are still available.[xiv]

These forces have begun to destabilize the market for individual health insurance by adding uncertainty and risk for insurers who sell health insurance plans to individuals, driving up insurance premiums and potentially reducing the pool of healthy people purchasing insurance. As healthy people leave the insurance market, only sicker patients remain. This means insurers have higher average health care costs per customer, which leads to higher premiums and further discourages healthy people from purchasing insurance. This market dynamic is sometimes referred to as an “insurance death spiral.”

There are a number of policies Oregon could consider to help limit premium increases, maintain enrollment by healthier individuals and stabilize the individual insurance market so that it remains a valid route for Oregonians to obtain health coverage.

- Adopt a state-level individual insurance mandate. This would require all Oregonians to have health insurance or pay a tax penalty, compelling healthier customers into the market, lowering the average premium, and maintaining a steady level of risk for insurers. Massachusetts, New Jersey, Vermont, and Washington, D.C., have all adopted their own individual insurance mandates. Tax revenue from individuals who opt to pay the penalty instead of purchasing insurance can be used to help further stabilize the insurance market.

- Explore a “public option.” A public option would allow individual consumers to purchase a government-supported health plan akin to the Oregon Health Plan, which is the state’s Medicaid insurance program. Consumers would pay premiums on an ongoing basis to help cover health care and administrative costs, and the state may need to subsidize premiums for some consumers. A public option could increase choice for consumers in counties with few options. Risks of a public option include driving private insurers out of some counties if the public option puts downward pressure on premiums, and splitting patients into healthy and unhealthy risk pools. No state has yet created a public option and Oregon would have to be a pioneer on this policy.

- Protect consumers who are not eligible for tax credits from premium increases. To cover federally mandated benefits that the federal government has stopped subsidizing, Oregon has allowed insurers to raise rates on benchmark insurance plans, enabling insurers to cover their costs and triggering higher federal tax credits for many consumers purchasing insurance on the exchange. However, consumers who earn too much to qualify for federal aid have had to pay more. Oregon could revise its rules so that premium increases are largely limited to consumers who receive federal tax credits. This approach is vulnerable to additional federal policy changes.

- Consider enhancements to Oregon’s reinsurance program to further limit how much insurers pay on behalf of consumers with especially high medical bills. Currently, Oregon’s program covers 50 percent of the medical bills for patients who purchased insurance in the individual market and who incur expenses between $95,000 and $1 million. Oregon could pursue changes to the program that might further reduce risk for insurers and enable them to charge lower premiums. For example, instead of or in addition to its current program, Oregon could focus on patients with potentially high-cost medical conditions and try to improve management of their health. Experience in Maine and Alaska suggests this could reduce rate increases and allow better management of care for high-risk patients.

- Shift control of Oregon’s online health care market to the state instead of the federal government’s online platform, HealthCare.gov. This could reduce costs for insurers. Oregon insurers will pay an estimated $25 to $30 million to the federal government in 2019 for using the federal platform, up from $16 million in 2018.[xv] A state-run platform could be cheaper. Nevada, for example, expects to save $5.5 million in the first year by switching to a state-run exchange.[xvi] In addition, full control of the online platform would enable the state to provide more effective outreach and assistance to individuals who need insurance, potentially increasing the number of people who successfully enroll.

Many of the steps that Oregon could take to stabilize the individual insurance market will be hard to maintain in the face of ever-increasing health care costs. To truly stabilize the individual health insurance market, maintain employer-based coverage, and keep government health care spending to a reasonable level, Oregon must broaden its efforts to address the underlying problem of high and rising health care costs. The state should seek opportunities to reduce health care spending by all payers in the state, while at the same time maintaining or improving the quality of care.

[i] Centers for Medicare & Medicaid Services, National Health Expenditure Data: Health Expenditures by State of Residence, June 2017, available at https://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/NationalHealthExpendData/NationalHealthAccountsStateHealthAccountsResidence.html.

[ii] Centers for Medicare and Medicaid Services, National Health Expenditure Data: Historical, 8 January 2018, available at https://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/NationalHealthExpendData/NationalHealthAccountsHistorical.html.

[iii] Kaiser Family Foundation, Marketplace Average Benchmark Premiums, 2014-2019, accessed 16 January 2019, at https://www.kff.org/health-reform/state-indicator/marketplace-average-benchmark-premiums/?currentTimeframe=0&sortModel=%7B%22colId%22:%22Location%22,%22sort%22:%22asc%22%7D.

[iv] Ibid. KFF looked up the cost for a 40-year-old in each county and weighted the results by county plan selections. 2019 data reflect approved rates.

[v] Internal Revenue Service, Questions and Answers on the Premium Tax Credit, 16 March 2018, archived at https://web.archive.org/web/20181230090102/https://www.irs.gov/affordable-care-act/individuals-and-families/questions-and-answers-on-the-premium-tax-credit.

[vi] Centers for Medicare and Medicaid Services, The “Metal” Categories: Bronze, Silver, Gold & Platinum, accessed 17 October 2018, archived at https://web.archive.org/web/20181017174557/https://www.healthcare.gov/choose-a-plan/plans-categories/.

[vii] Louise Norris, “What Is a Benchmark Plan Under the ACA?” VeryWell Health, 9 April 2018, archived at https://web.archive.org/web/20190320000848/https://www.verywellhealth.com/under-the-aca-what-is-a-benchmark-plan-4160065.

[ix] In December 2017, Congress passed the Tax Cuts and Jobs Act and eliminated the individual mandate penalty, effective January 1, 2019.

[x] Regence BlueCross BlueShield of Oregon, Filing for H16I Individual Health – Major Medical/H16I.005A Individual – Preferred Provider (PPO), SERFF Tracking #: RGOR-131494722, accessed 13 March 2019 at https://www4.cbs.state.or.us/exs/ins/rates2/index.cfm?B64=nZzVWZjFGdvljbo12bl1nLoN3bfdGZj9WbtdCd0Z1az9mcfZmZslWan52XvRzYx0%0A%0DDMxAQO%3D%3D, and Health Net Health Plan of Oregon, Inc., Filing for H16I Individual Health – Major Medical/H16I.005C Individual – Other, SERFF Tracking #: HNOR-131466265, accessed 13 March 2018 at https://www4.cbs.state.or.us/exs/ins/rates2/index.cfm?B64=nZzVWZjFGdvljbo12bl1nLoN3bfdGZj9WbtdCd0Z1az9mcfZmZslWan52XvRzYx0%0A%0DDMwAQO%3D%3D.

[xi] Jeff Manning, “Oregon’s Second Health Insurance Co-op to Be Liquidated,” The Oregonian/OregonLive, 8 July 2016, archived at https://web.archive.org/web/20190320001047/https://www.oregonlive.com/business/2016/07/oregons_second_health_insuranc.html.

[xii] Slightly under half of individuals who obtain insurance through the individual market do not receive a tax credit to help reduce their monthly premiums. Seventy-four percent of participants in the exchange qualified for a tax credit in 2018, per Department of Consumer and Business Services, Oregon Health Insurance Marketplace: 2017 Annual Report, 15 April 2018, archived at https://web.archive.org/web/20190320001143/https://www.oregonlegislature.gov/salinas/HealthCareDocuments/3.%20Marketplace-Annual-Report%202017%20-%20Released%204.15.18.pdf. In 2017, 3.7 percent of Oregonians obtained insurance through the exchange and 1.5 percent bought individual plans off the exchange, per Oregon Health Authority, 2017 Oregon Health Insurance Survey: Early Release Results, 5 December 2017, archived at https://web.archive.org/web/20190320001244/https://www.oregon.gov/oha/HPA/ANALYTICS/InsuranceData/2017-OHIS-Early-Release-Results.pdf.

[xiii] Louise Norris, “The Problem with Association Health Plans,” Healthinsurance.org, 1 June 2018, archived at https://web.archive.org/web/20180919122003/https://www.healthinsurance.org/blog/2018/06/01/the-problem-with-association-health-plans/.

[xiv] Linda Blumberg, Matthew Buettgens and Robin Wang, Urban Institute, Updated: The Potential Impact of Short-Term Limited-Duration Policies on Insurance Coverage, Premiums and Federal Spending, March 2018, archived at https://web.archive.org/web/20181129161531/https://www.urban.org/sites/default/files/publication/96781/2001727_updated_finalized.pdf, and Jeff Manning, “For Oregonians, Rate Hikes Ease But Still Sting: 2019 Insurance Guide,” The Oregonian/OregonLive, 28 October 2018, archived at https://web.archive.org/web/20190320041726/https://www.oregonlive.com/business/2018/10/in_oregon_rate_hikes_ease_but.html.

[xv] Markian Hawryluk, “Oregon Could Relaunch State Insurance Exchange,” The Bulletin, 13 May 2018, archived at https://web.archive.org/web/20180710035141/https://www.bendbulletin.com/localstate/6232435-151/oregon-could-relaunch-state-insurance-exchange.